How to Send Money to India Without Tax: NRE vs NRO Rules for Large Transfers

Complete guide for NRIs sending large amounts from US to India tax-free. NRE vs NRO accounts, FEMA compliance, and avoiding common transfer mistakes.

Posted by

Admin

Posted at

Banking & Remittances

Posted on

Apr 1, 2025

Sending large amounts from the US to India? You're not alone. Thousands of NRIs find it challenging to transfer money to India without tax or delay. In this guide, we'll walk through the NRE/NRO account options, 15CA/CB forms, FEMA rules, and how to avoid common mistakes that trigger tax notices or blocked transfers.

You can legally transfer large sums (even over $50,000) to India, if you do it right.

Most Popular Questions on Reddit

1. The Tax-Free Transfer Method

The most tax-efficient way for NRIs to send money is through an NRE (Non-Resident External) account. Funds remitted here are fully repatriable and tax-free in India.

However, if you send money to a normal resident savings account, you may trigger TDS or compliance scrutiny under FEMA.

Quick Summary:

Send to NRE = No tax, no limit, minimal compliance, no delay

Send to resident savings account = Tax flags, FEMA breach, possible notices

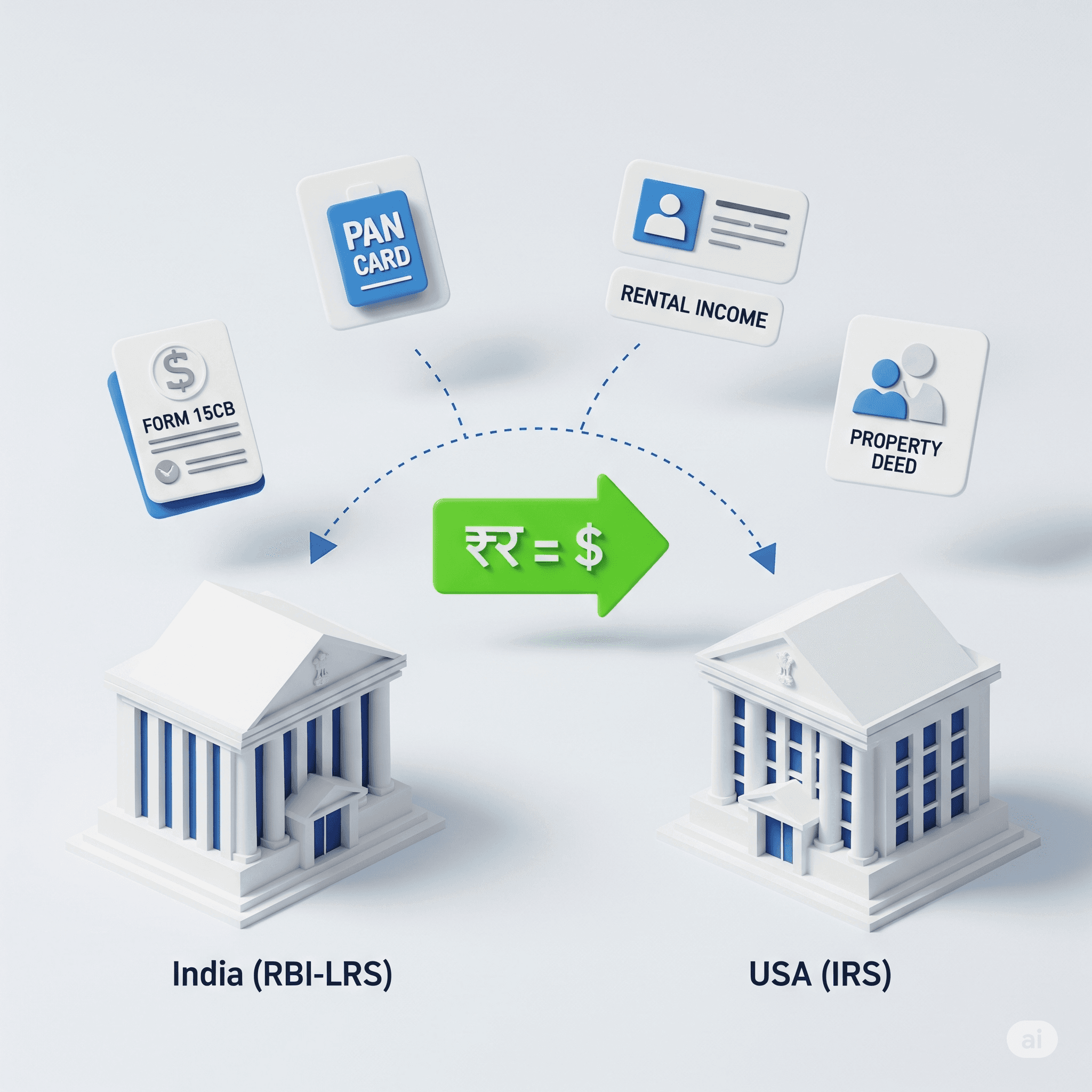

2. NRE vs NRO for Large Transfers

NRE Account: Best for foreign income. No Indian taxes, fully repatriable. Ideal for large bank-to-bank SWIFT transfers. No daily/monthly limits like transfer services.

NRO Account: Best for Indian income like rent or dividends, subject to taxes. Transfers in or out need 15CA/15CB and are capped at $1 million/year.

Avoid resident accounts: FEMA does not allow NRIs to maintain or transfer directly to personal resident savings accounts.

Make sure to discuss and finalize the currency conversion rate with the Indian bank before wiring funds.

3. How to Do a Clean Bank-to-Bank Transfer

Here's what works best:

Use your US bank's SWIFT wire to transfer to an Indian NRE account

Confirm the purpose code with the receiving Indian bank (e.g., P1301 for family savings)

Ask the Indian bank to issue a Foreign Inward Remittance Certificate (FIRC)

Avoid remittance apps (Wise, Remitly etc.) for large transfers, they have limits and weaker documentation trails.

4. Will I Get a Tax Notice for Large Transfers?

Not always, but if you don't have paperwork, you're at risk.

Keep these documents:

Source of funds (US salary slip or W2, bank statements)

Transfer receipt (SWIFT confirmation, NRE deposit)

FIRC + TRC (Tax Residency Certificate, if needed)

These help defend against Section 148A notices, Black Money Act queries, and FEMA violations.

Common Mistakes to Avoid

Sending money to a resident account - FEMA violation for NRIs

Using Remitly/Wise for large transfers

Not filing 15CB properly for NRO transfers

Using wrong purpose codes

Ignoring FATCA/FBAR reporting in your home country

What Is FEMA and Why It Matters

FEMA is India's law governing foreign exchange. Most NRIs unknowingly violate FEMA by:

Keeping resident accounts after moving abroad

Transferring money to family-owned resident accounts

Not reporting large transactions properly

Confused About 15CA/15CB Forms?

Form 15CA: Declaration of remittance by the sender Form 15CB: Certification by a CA that taxes are paid or not applicable

Most delays happen because the CA doesn't file 15CB correctly. This is the #1 bottleneck we see for NRIs.

Need help with compliant money transfers? Consult our NRI banking experts with a free 15 minute consultation call.