From India to the US: How to Securely Transfer Funds Without Breaking the Law

Complete guide for Indians moving to the US on legal fund transfers. RBI rules, LRS limits, and documentation requirements to avoid FEMA violations.

Posted by

Admin

Posted at

Banking & Remittances

Posted on

Nov 21, 2024

For Indians moving to the US, one of the most confusing, and risky, steps is figuring out how to legally bring your money with you. From family gifts and property sale proceeds to rental income, there are strict rules around how and how much you can send abroad. This guide breaks it down simply.

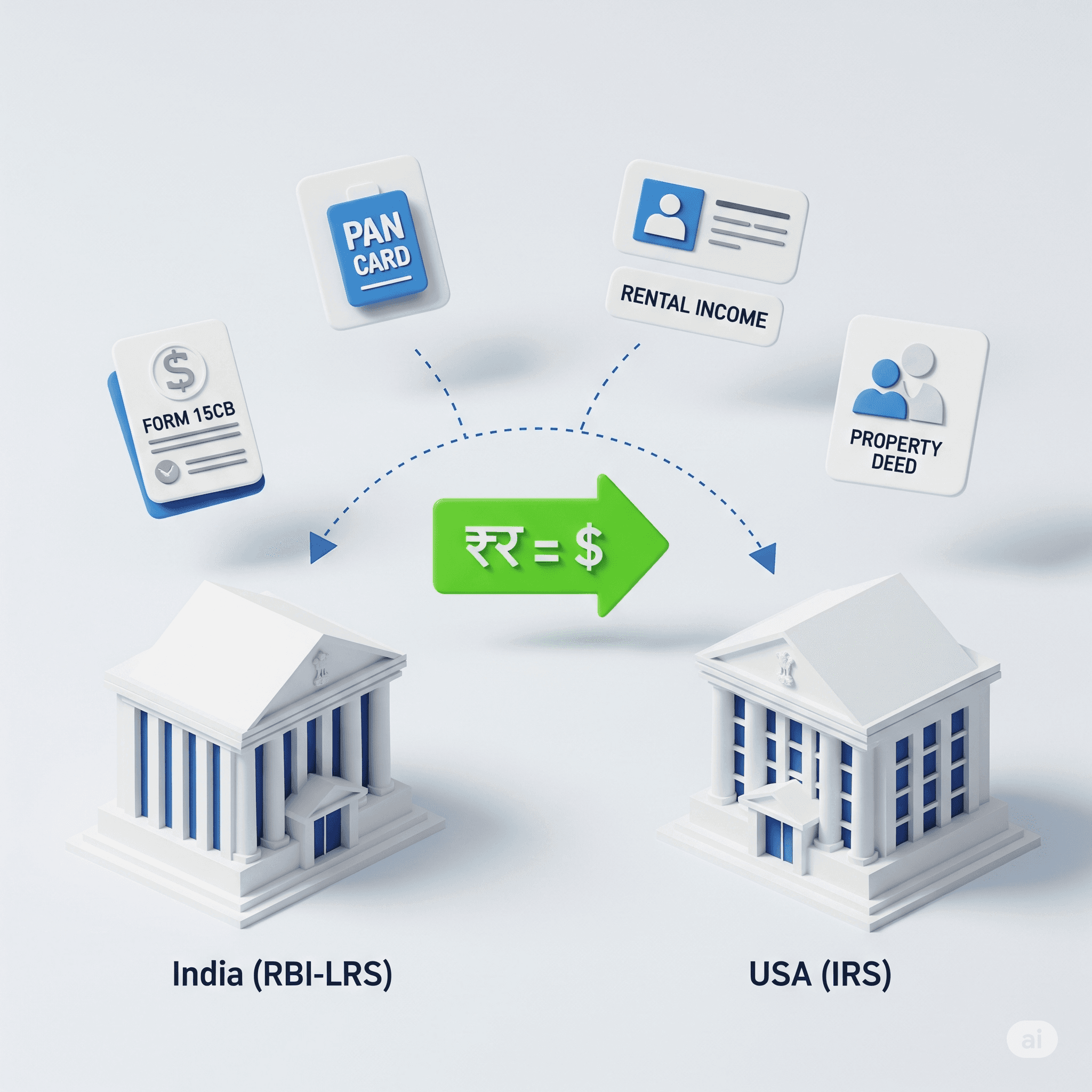

The Reserve Bank of India (RBI) permits Indian residents to remit up to USD 250,000 per financial year under the Liberalised Remittance Scheme (LRS). But depending on your residency status, source of income, and purpose of remittance, different documentation and limits apply.

Key Things to Know

1. Gifts vs Income

Sending money as a "gift" to your NRI self (from parent account to your foreign account) has different tax and compliance implications compared to remitting your Indian rental income or capital gains.

2. Repatriation of Sale Proceeds

If you've sold property in India and want to transfer the proceeds to the US, you'll need proper tax clearance, CA certification (Form 15CB/15CA), and possibly RBI approval.

3. Using LRS Channels

You must route remittances through authorised dealers (banks), not informal hawala methods, to ensure legal compliance.

Avoid These Common Mistakes

1. Using Undocumented Routes

Many NRIs unknowingly violate FEMA or Income Tax laws by using relatives, middlemen, or untracked forex services.

2. Mismatched Purpose Codes

If the purpose of transfer is incorrectly declared (e.g. marking "gift" instead of "property sale"), it can flag your account for audit or rejection.

3. Neglecting Tax Filing in India

Even if your income is being moved abroad, Indian taxes might still apply unless you've properly filed and declared it.

Settleline's NRI Remittance Playbook

What we do for clients:

Evaluate source of funds: salary, gift, rent, property, startup exit

Create a repatriation roadmap with CA-certified documentation

File Form 15CA/CB with the right purpose codes

Help with RBI compliance, if applicable

Coordinate with US-side CPA if FBAR/FATCA applies

Ready to transfer funds legally? Book a free consultation with our experts.