Avoid These Mistakes When Moving Abroad With Indian Assets

Essential checklist to prepare your Indian assets before relocating abroad. Bank account conversions, documentation, and tax planning to avoid costly NRI mistakes.

Posted by

Admin

Posted at

Migration & Compliance

Posted on

Feb 4, 2025

If you're planning to move abroad, don't just book your flights, organize your Indian assets first. From frozen bank accounts to tax penalties, thousands of NRIs face issues simply because they didn't prepare. Here's what to fix before you relocate.

Red Flags

1. Not Converting Your Bank Accounts Before Leaving

Once you become a non-resident, your Indian savings account becomes non-compliant. Banks can freeze your account or block transactions.

Solution: Convert your account to an NRE (Non-Resident External) or NRO (Non-Resident Ordinary) account. This helps you legally manage India-side earnings like rent or dividends and also makes remitting funds abroad much easier.

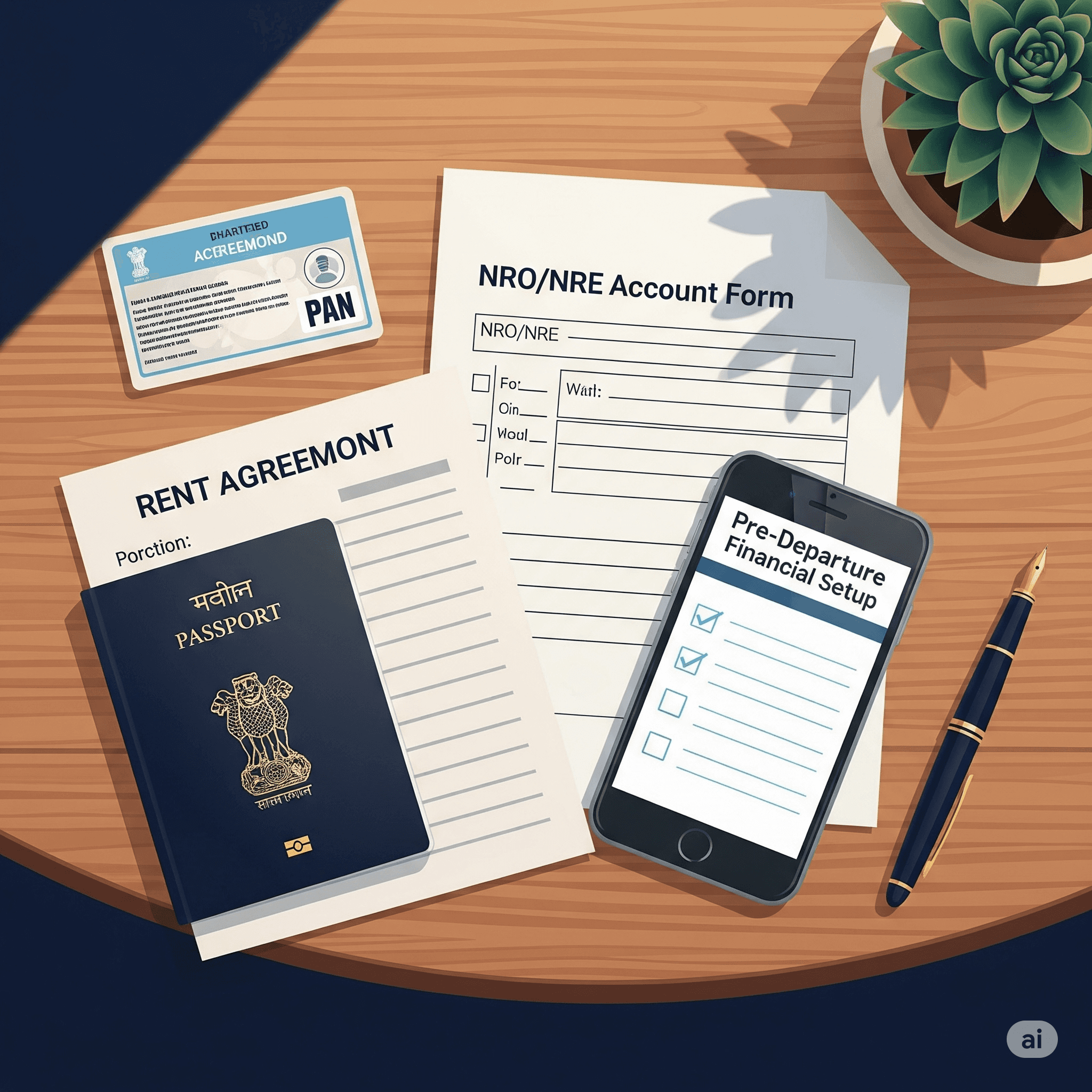

2. Leaving Behind Disorganized or Incomplete Documents

Most NRIs don't have digital access to important paperwork - property title deeds, PAN details, tax returns, or Power of Attorney documents. If something goes wrong while you're abroad, handling it from overseas becomes a nightmare.

Solution: Scan and store everything securely. And nominate a trusted PoA holder to act on your behalf for things like property sales, rentals, or legal claims.

3. Trying to Repatriate Funds Without a Plan

You can't just wire large sums from India to your new country. FEMA rules require documentation, tax clearance, and approval in many cases.

Solution: Talk to a CA or repatriation expert. Ensure your income trail is clean, especially for property sales, rent, or mutual fund redemptions. Know which forms (like 15CA/15CB) are required and how to avoid TDS issues.

4. Ignoring Tax Residency and Double Taxation

Even after you move, India might still consider you a resident for tax purposes if you stay more than 182 days in the financial year. This could mean paying taxes in both countries.

Solution: Before you leave, consult a CA who understands cross-border tax laws and DTAA agreements. If you're liquidating assets or claiming deductions, the timing of your move can affect your tax bill.

Planning your move abroad? Get expert guidance on asset preparation and compliance.