Mid-Year Return to India: Complete Tax Filing Guide for Both Countries

Mid-year return to India creates dual filing obligations in both countries. Understand RNOR status, dual-status taxpayer rules, and new Income Tax Bill 2025 implications for optimal tax planning.

Posted by

Admin

Posted at

Migration & Compliance

Posted on

Aug 19, 2025

Updated for FY 2025-26 under the new Income Tax Bill 2025

Returning to India in the middle of a tax year creates dual filing obligations that catch most people unprepared. Understanding your tax status in both countries and filing correctly can save thousands in unnecessary taxes and penalties.

Understanding Your India Tax Status

Your residential status in India determines what income gets taxed, making timing crucial for your return.

Non-Resident (NR) Status

Qualification: Less than 182 days in India during the financial year Tax Implication: Only Indian-sourced income is taxable Benefit: No tax on foreign salary, investments, or other overseas income

Special Rule: If your Indian income exceeds ₹15 lakh and you stay 120-181 days, you may still be considered resident.

RNOR (Resident but Not Ordinarily Resident) Status

Qualification Criteria (Any One):

Non-resident in 9 out of 10 preceding years

Stay ≤ 729 days in past 7 years

Deemed resident but not taxed abroad

Tax Advantage: Only Indian-sourced income taxable; foreign income kept abroad remains tax-free Duration: Typically 2-3 years after return Strategic Value: Significant tax savings on overseas investments, salary, RSUs during this period

ROR (Resident and Ordinarily Resident) Status

When Applied: Resident in India and fails RNOR qualification tests Tax Implication: Global income taxable in India Impact: Most expensive status for those with substantial foreign assets

New Income Tax Bill 2025 Implications

Starting FY 2025-26, higher tax slabs make RNOR planning even more valuable:

New Tax Slabs:

₹0 - ₹4 lakh: 0%

₹4 - ₹8 lakh: 5%

₹8 - ₹12 lakh: 10%

₹12 - ₹16 lakh: 15%

₹16 - ₹20 lakh: 20%

₹20 - ₹24 lakh: 25%

Above ₹24 lakh: 30%

Planning Impact: With change in slabs, RNOR status & planning becomes more valuable for high-income returnees.

US Tax Filing Requirements

Dual-Status Taxpayer Rules

When you leave the US mid-year, you become a "dual-status taxpayer" with different rules for each period.

Resident Period (January to departure date):

All worldwide income reported

Standard deductions and exemptions apply

Taxed as US resident

Non-Resident Period (Departure date to December 31):

Only US-sourced income taxable

Filing Requirements

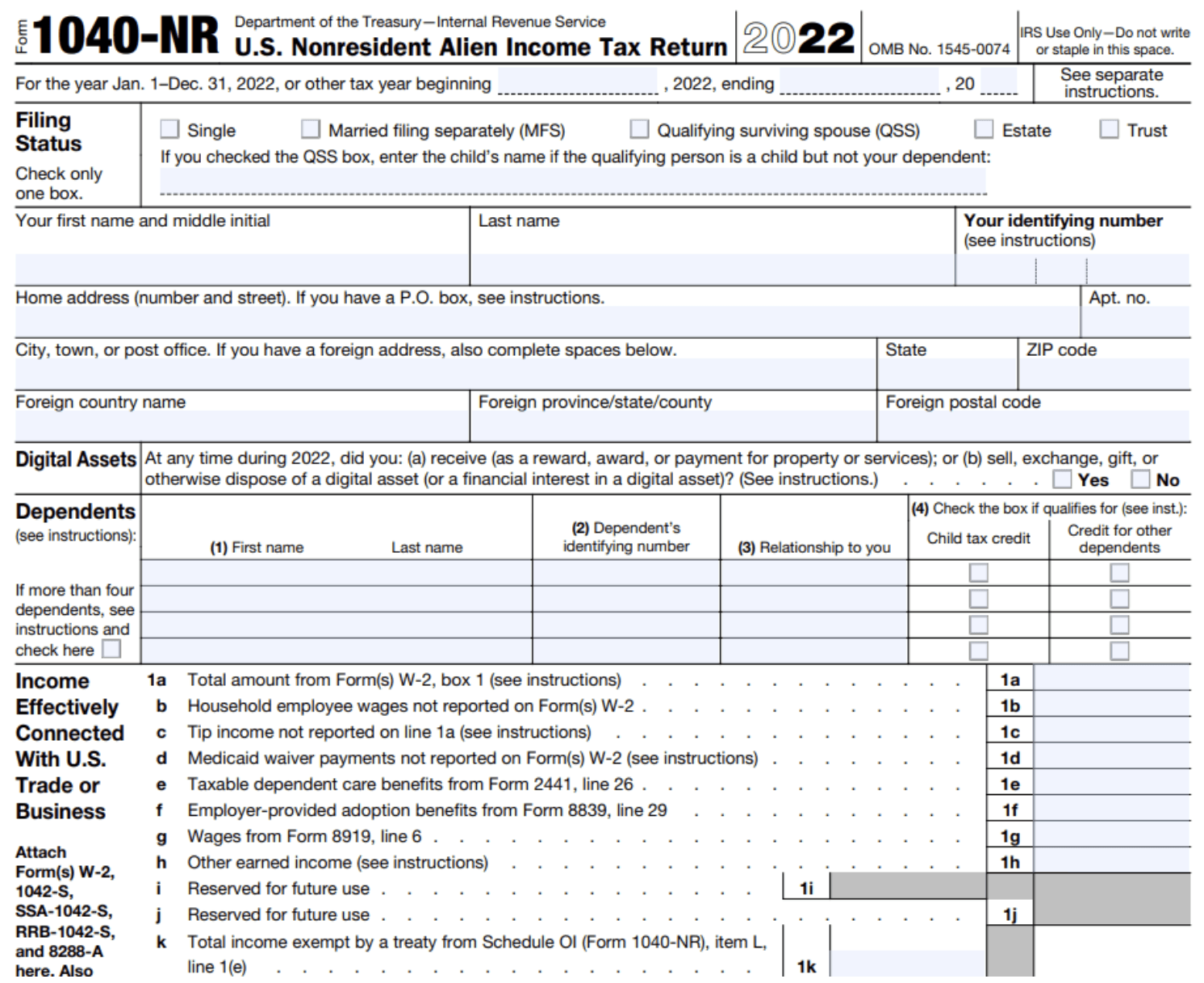

Form 1040NR: Required for the non-resident portion Dual-Status Statement: Must attach explaining the transition

Important: Some states consider you resident until you formally break ties, regardless of physical presence.

India Filing Requirements

Residential Status-Based Obligations

If Non-Resident:

File only if you have Indian-sourced income

Use appropriate ITR form based on income types

No global income reporting required

If Resident/RNOR:

Mandatory filing if total income exceeds basic exemption

File ITR-2 for salary + capital gains

File ITR-3 if you have business/professional income

Schedule FA Compliance

Mandatory Disclosure: All foreign assets must be reported in Schedule FA

Applies To: Any foreign bank account, investment, or asset

Penalty: ₹10 lakh per year under Black Money Act for non-disclosure

Critical: Required even if account has zero balance

Strategic Planning Opportunities

RNOR Optimization

Best Practice: Time your return to qualify for RNOR status Benefit: Foreign income not remitted to India stays tax-free Duration: Maximize the 2-3 year RNOR window for major transactions

Example Applications:

RSU vestings and sales

US stock portfolio liquidation

401K distributions

Foreign rental income

Common Mistakes to Avoid

Missing US State Filing Requirements Assuming departure from US automatically ends state tax obligations.

Poor Schedule FA Compliance Failing to report foreign assets in India filing. The ₹10 lakh penalty applies even for zero-balance accounts.

Incorrect DTAA Claims Filing for treaty benefits without proper documentation or understanding of specific treaty provisions.

Suboptimal Timing Returning without considering the impact on RNOR qualification and tax optimization opportunities.

Professional Guidance Required

Mid-year returns involve complex interactions between:

Dual-status filing requirements in the US

Residential status determination in India

DTAA treaty benefit optimization

New Income Tax Bill 2025 implications

Multi-state compliance obligations

The timing of your return affects years of future tax obligations. Professional guidance ensures optimal structuring and compliance across both jurisdictions.

Get Expert Cross-Border Filing Support

Our integrated US-India tax team specializes in dual-country filing requirements for mid-year returnees. We handle the complexity of coordinating filings across both tax systems while optimizing your residential status and treaty benefits.

Free 15-minute consultation to review your specific mid-year return situation and filing requirements.

📞 Contact Settleline: +91-9821844770

🌐 Schedule consultation: settleline.com/contact

Disclaimer: This article provides general information about mid-year return tax filing for educational purposes. Tax laws are complex and change frequently. Always consult with qualified tax professionals for advice specific to your situation. The new Income Tax Bill 2025 provisions mentioned are based on the bill as passed by Parliament and subject to implementation rules.